What are unit trusts?

Unit trusts are defined by HMRC as a UK-resident, collective investment scheme funded by the contributions of investors. They are generally invested in shares, bonds, property and currency, and are often professionally managed.

The trust’s pool of investments is managed by the trust fund manager, though someone known as a trustee is the one who holds custody of the investments on behalf of the investors.

The investment pool is divided into equal portions called units. These units are then issued to investors, who are known as the trust beneficiaries or unitholders, at a price reflective of the current market value of the underlying investment.

What are the different types of unit trust?

Unit trusts with UK-resident trustees will either be Authorised Unit Trusts (AUTs) or Unauthorised Unit Trusts (UUTs). AUTs are authorised and regulated by the UK Financial Conduct Authority (FCA) and will fall into one of five categories defined by the financial body.

In contrast, UUTs are not authorised or regulated by the UK FCA. Instead, an UUT fund is governed by the requirements of the instrument constituting the scheme. Because of this, UUTs can often access a wider range of investments than AUTs but cannot be marketed to the general public.

AUTs and UUTs will either be open-ended or closed-ended funds. If the trust is open-ended, then the fund manager can issue and redeem units at any time. In closed-ended funds, there is a fixed number of units so there are restrictions on when a fund manager can issue or redeem units.

How do they work and make money?

All unit trust investors hold equal rights in proportion to their investment. These units are bought and sold directly from the manager of the unit trust. They are not traded as they are not listed shares.

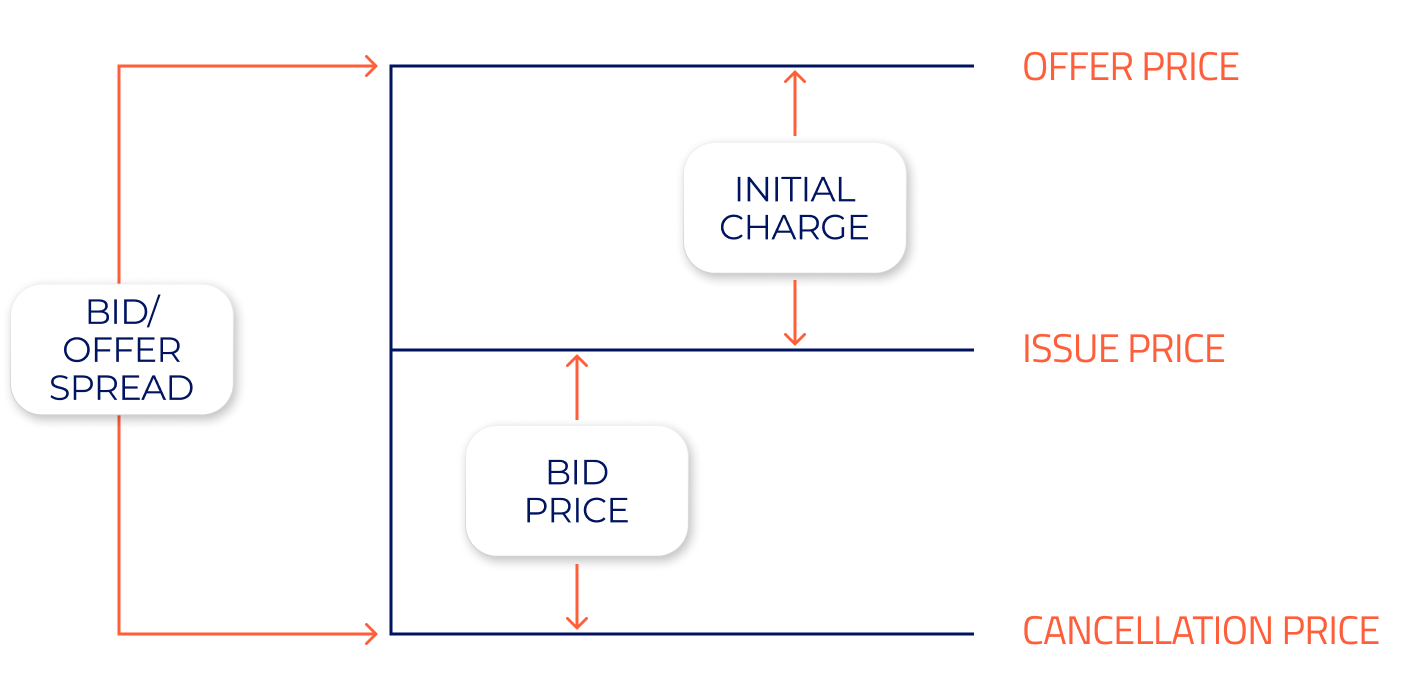

The price of units is set by the manager and is unaffected by market movements. Instead, the price of a unit is determined by considering the value of the underlying investments, the number of units issued and the cost of any liabilities.

A fund manager makes a profit through the difference between the offer price and the bid price of the portfolio. This is known as the bid/offer spread. Though it may seem like a straightforward calculation, there are many different factors that will influence the bid/offer spread.

The offer price is the cost to the fund of purchasing the entire portfolio, and the bid price is the proceeds of selling the entire portfolio. These prices are then apportioned to be per unit. The person buying units in a unit trust will pay the offer price and the person selling their units in a unit trust will receive the bid price.

How are unit trusts taxed?

AUFs themselves do not pay tax on the income and gains they make. Instead, HMRC will tax investors in the trust on their proportion of the income generated, whether this has been distributed to them or not.

There are two main taxes investors in unit trusts will be concerned with: income tax and capital gains tax. The amount of tax due will depend on the type of assets the fund is invested in and the growth of these investments. Stamp duty is not levied on purchases of units, though the unit trust will have to pay stamp duty on its purchases of UK shares.

Interest vs Dividends

If a unit trust is more than 60% invested in interest-bearing assets, such as gilts or bonds, any distributions from the trust are considered to be interest payments and therefore will be taxed as income.

Any interest payments an investor receives, up to £1,000, will be taxed at 0% if they are a basic rate taxpayer. Past this £1,000 allowance, for a basic rate taxpayer, the distributions will be taxed at 20%. If the investor is entitled to the starting rate for savings, then potentially up to an additional £5,000 will be tax free.

Higher rate taxpayers will only be taxed at 0% for the first £500 they receive in distributions, due to their lower personal savings allowance. Past this allowance, any distributions they receive will be taxed at 40%. As there’s no personal savings allowance for additional rate taxpayers, they will be taxed at 45% on any distributions they receive.

Things are different if 60% or less of the unit trust is invested in interest-bearing assets. In this scenario, distributions from the trust will be treated as dividends and taxed accordingly.

UK residents are entitled to a £500 annual dividend allowance, meaning any distributions up to this amount will be taxed at 0%. Past this £500 allowance, investors will be taxed on distributions according to their marginal tax rate. For basic rate taxpayers this would be 8.75%. For higher and additional rate taxpayers, this would be 33.75% or 39.35%, respectively.

Accumulation vs Income

Unit trusts generally offer two types of unit class: income units or accumulation units. Income units will pay regular distributions to investors. Accumulation units, meanwhile, will reinvest these distributions to grow the value of the trust.

As already discussed, investors will be subject to different taxes depending on whether their trust’s distributions are seen as interest or dividend payments. It is important to note that any income from a unit trust is always taxable, regardless of whether it is actually distributed to an investor or simply reinvested. It is therefore important to know how much of the unit trust is invested in interest-bearing assets.

Capital gains tax

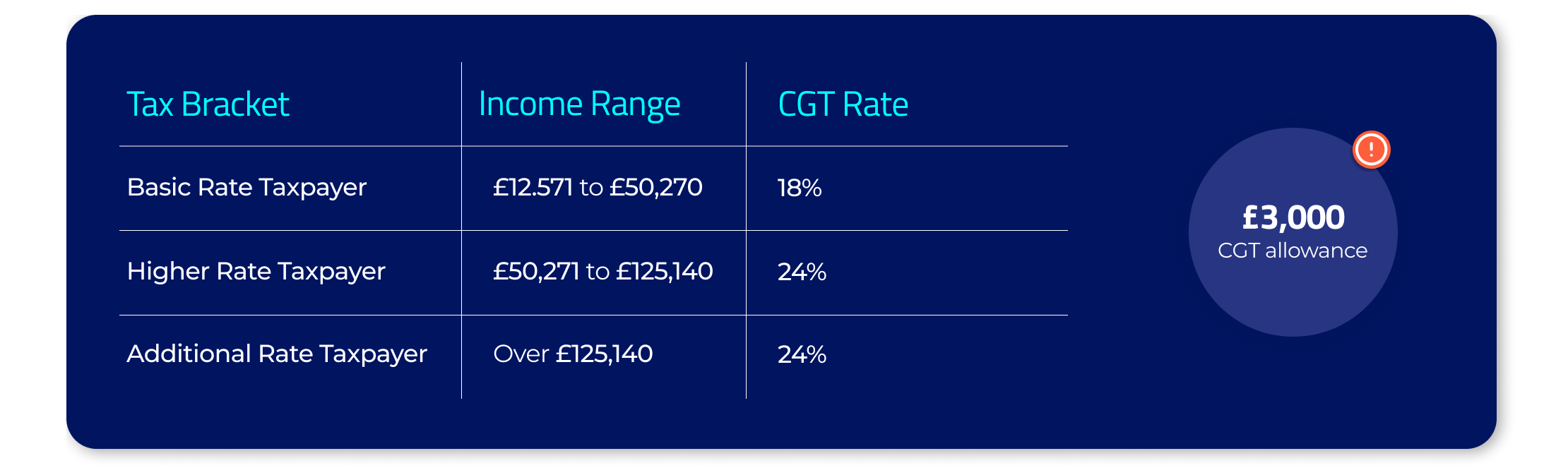

Regardless of whether an investor has opted for an accumulation or income-based unit trust, they will be subject to capital gains tax when they realise a gain on their investment. This can include the investor making a partial withdrawal or transferring their investment to a different unit trust.

All UK-resident investors are entitled to a tax-free annual exemption of £3,000. This means they will only be liable to capital gains tax on gains which exceed this amount. The investor will then be taxed according to their income tax band. The capital gains tax (CGT) rate for basic rate taxpayers is 18% and 24% for higher and additional rate taxpayers.

Unit trusts can be held within tax-free wrappers, such as an Individual Savings Account (ISA). So, as long as the investor hasn’t exceeded their £20,000 ISA allowance, any income or gains resulting from a unit trust inside an ISA will remain tax free.

Equalisation payments

How are they taxed?

Unit trusts tend to have fixed dates on which they pay distributions. They tend to also have fixed dates which determine whether an investor will be eligible to receive these distributions.

Investors will be entitled to the unit trust’s income in a given distribution period if they hold units at the trust’s dividend record date (the day before its ex-dividend date). This means that even if the unit trust’s income arose before an investor had purchased their units, they will still be entitled to an equal proportion of this income so long as they hold units at this date.

However, to ensure fairness, unit trusts will operate an equalisation scheme. This splits into two groups, as determined by the dividend record date: those who bought units before the distribution period and those who bought units during the distribution period.

Units bought before the distribution period as referred to as Group 1 units, and units bought during are referred to as Group 2 units. Investors who hold Group 2 units will have been required to pay an extra amount to purchase their units, on top of the standard price. This extra amount is the amount of income earned by the unit trust to date since its last distribution date.

When the unit trust’s next distribution is paid, the investor holding Group 2 units will receive the same amount of cash per unit as the investor with Group 1 units, but part of their cash will be a refund of the extra amount they paid for their units. This is known as an equalisation payment.

An equalisation payment is not considered income, nor is it treated as a capital distribution. This is because it is seen as a return of the initial price paid. As a result, it is deducted from the price paid when calculating the chargeable gain on the eventual disposal of an investor’s holding.

An investor will still be subject to income tax on the distribution they receive. However, the amount chargeable to income tax will be adjusted to take the equalisation payment into account.

How CGiX handles equalisation payments

CGiX automatically applies the correct Group 1 or Group 2 designation to units based on when they were purchased within each account period.

Group 1 will be applied to units held for the full account period and Group 2 will be applied to units purchased outside the account period. When both new and existing units are present, CGiX will ensure the correct proportional application of Group 1 and Group 2 for the investor.

If an investor holds Group 2 units, CGiX will take the equalisation payment into account when calculating their tax liability.

Talk to one of our experts to find out what else CGiX can do for you.